How Mortgages Are Changing in 2025: Rates, Terms, Requirements, and Practical Tips

Discover the latest mortgage trends for the second half of 2025: what’s changing, new opportunities, and strategies for a smart choice.

General Scenario – Monetary Policy and Mortgage Impact

In 2025, the European Central Bank initiated a series of interest rate cuts, with the official marginal lending rate set at 2.00% as of June.

The main effect: the Euribor – the benchmark for variable-rate mortgages – has dropped below 2%, averaging around 1.8–2% in the first half of the year.

Forecasts for the second half of 2025 suggest a further decrease:

• 3M Euribor could fall to 1.74%, likely fluctuating between 1.5% and 1.8% by year-end.

Updated Rates – Second Half 2025

• Variable-Rate Mortgage:

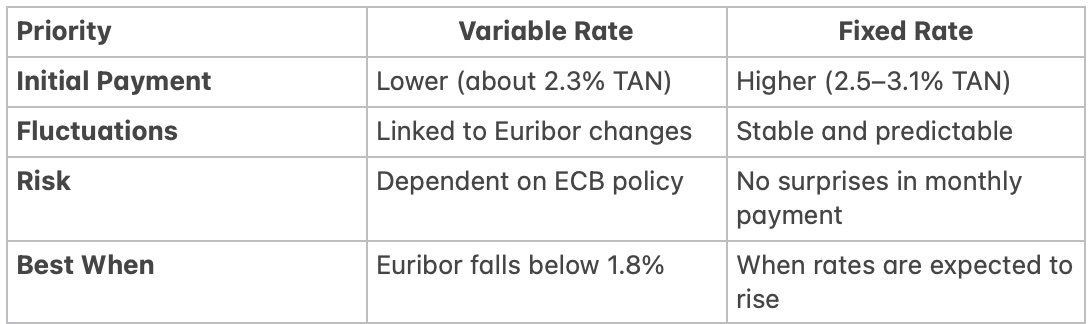

• As of June, the average fixed rate (TAN) is about 2.32–2.96% (TAEG included), lower than early 2025.

• Thanks to lower ECB rates, a €126,000 variable mortgage could see monthly payments drop by €17–21 by year-end.

• Fixed-Rate Mortgage:

• Average TAN between 2.19% and 3.1%; green mortgages as low as 2.19% TAN – 2.41% TAEG.

Market Trends and Demand

• In the first half of 2025, mortgage applications grew by +22%, with higher average amounts than 2024 (about €150,732).

• 41.3% of requests are for terms of 25–30 years, allowing for lower monthly payments.

Fixed or Variable? What to Consider

Opportunities: Switching and Green Mortgages

• Variable-rate mortgages may offer monthly savings of around €20, while switching to a fixed-rate could bring savings up to €40 per month (e.g., payment dropping from €666 to €579).

• Banks offer competitive fixed rates, often between 2.4–2.7%, with special green deals.

Practical Tips

• Assess your timeline: If you’ll stay in the house for 5–10+ years, fixed rates can protect you from market swings.

• Always compare offers: Use up-to-date comparison tools (Facile.it, MutuiOnline) to check all terms and promotions.

• Look for green options: They often come with lower rates for energy-efficient renovations.

• Consider switching: Moving from variable to fixed can secure a predictable payment.

The Takeaway

In the second half of 2025:

• Variable rates are falling: 3M Euribor toward 1.7–1.8%, meaning payments are down by €17–21 per month.

• Fixed-rate mortgages remain competitive: TAN around 2.2–2.7%.

• Choosing fixed or variable depends on your risk tolerance and your desire for stable payments.